Medicare Part D Substitution: What You Can and Can't Swap Under Current Rules

When your pharmacist hands you a different pill than what your doctor prescribed, it’s not a mistake - it’s Medicare Part D substitution. But not all substitutions are allowed, and not all plans let you swap drugs the same way. If you’re on Medicare and take prescriptions, understanding how substitution works could save you hundreds - or even thousands - of dollars a year.

What Is Medicare Part D Substitution?

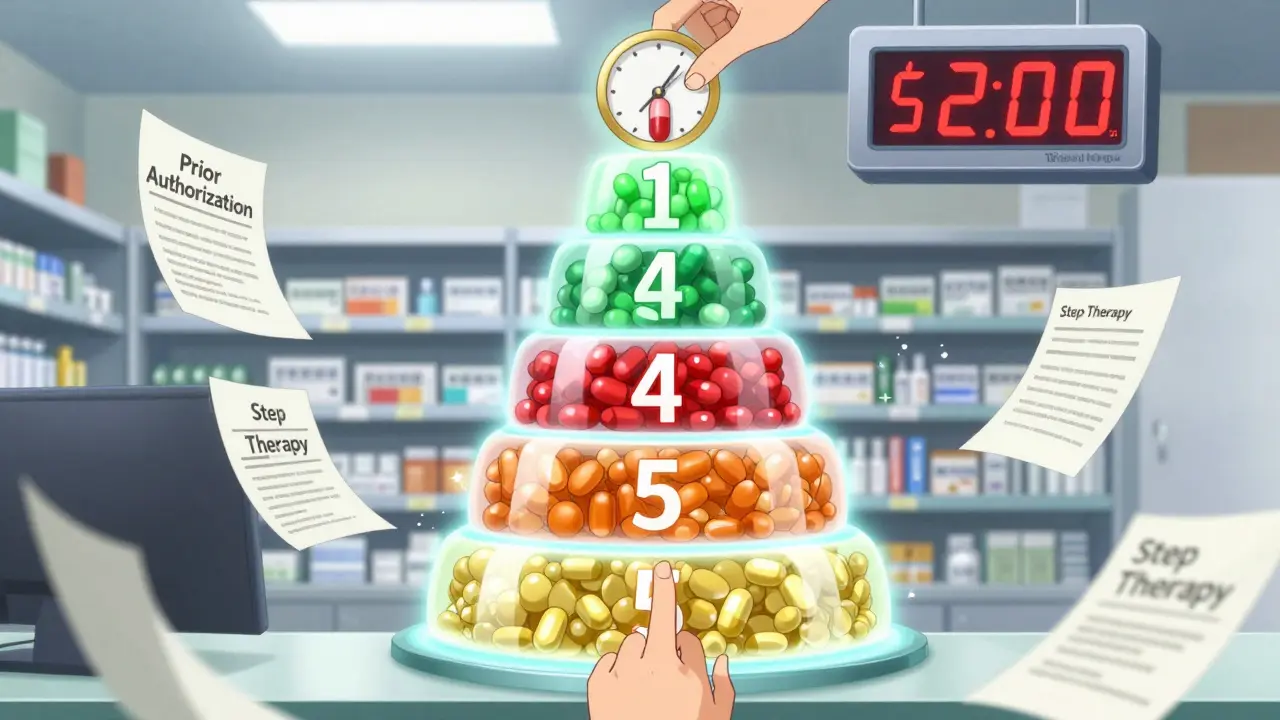

Medicare Part D substitution means switching one drug for another - usually a cheaper version - when filling a prescription. This isn’t random. It’s governed by strict rules set by your plan and the federal government. The goal? Lower costs without hurting your health. Most substitutions happen between generic and brand-name drugs. For example, if your doctor prescribes Lipitor (a brand-name cholesterol drug), your pharmacist might give you atorvastatin - the generic version - unless your doctor says no. This is legal and common. But substitution doesn’t always mean swapping within the same drug class. Sometimes, your plan might push you from one brand to another brand in the same therapeutic group. That’s called therapeutic interchange, and it’s trickier. Here’s the catch: your plan decides what can be swapped. Every Medicare Part D plan has a formulary - a list of covered drugs - and each drug is placed on a tier. The lower the tier, the less you pay. Generics are usually on Tier 1. Brand-name drugs? Often Tier 3 or 4. If your drug gets moved to a higher tier, your out-of-pocket cost could jump from $10 to $100 overnight.How Formularies Control What Gets Substituted

Your Part D plan’s formulary is the rulebook. It’s not the same across plans. One plan might cover Humalog insulin and let you swap it for a cheaper biosimilar. Another might not cover it at all. That’s why you can’t assume your current drug will be covered - even if it was last year. In 2025, most Part D plans use a five-tier system:- Tier 1: Preferred generics (lowest cost)

- Tier 2: Non-preferred generics

- Tier 3: Preferred brand-name drugs

- Tier 4: Non-preferred brand-name drugs

- Tier 5: Specialty drugs (highest cost)

The $2,000 Out-of-Pocket Cap Changes Everything

Starting January 1, 2025, the Medicare Part D “donut hole” disappeared. That’s not just a name change - it’s a financial reset. Before 2025, once you hit $4,430 in total drug spending, you entered the coverage gap. You paid 25% of the cost for brand-name drugs and 37% for generics. That gap created a weird incentive: if your drug was expensive, your plan might push you to a cheaper alternative before you hit that threshold. Now? Once you hit $2,000 in out-of-pocket spending for covered drugs, you enter catastrophic coverage. After that, you pay nothing for the rest of the year. That’s huge. What does this mean for substitution? Less pressure to switch drugs early. If you’re close to the $2,000 cap, your plan may be less likely to force a swap - because you’re about to pay nothing anyway. But if you’re still in the initial coverage phase (after your $590 deductible but before $2,000), substitution becomes more aggressive. Plans still want to save money, and they’ll push you toward lower-tier drugs to keep your spending under the cap.Therapeutic Interchange: When a Different Drug Is Pushed

Sometimes, substitution isn’t just swapping a generic for a brand. It’s swapping one brand for another brand - even if they’re not identical. This is therapeutic interchange. Example: You take Ozempic for diabetes. Your plan doesn’t cover it, but it does cover Trulicity - another GLP-1 drug. Your plan may require you to try Trulicity first. If it doesn’t work, your doctor can appeal. But if you’re stable on Ozempic and it’s working well, forcing a switch could hurt your health. This is where prior authorization matters. Your doctor has to prove to the plan that the alternative won’t work for you. That takes time. And if you’re not prepared, you might run out of medication. Humana, for example, caps insulin costs at $35 for a 30-day supply - no matter what plan you’re on. That’s a direct policy to prevent substitution pressure on high-risk medications. But not all drugs have those protections.

How to Avoid Surprises With Substitution

You don’t have to guess what your plan will allow. Here’s how to stay in control:- Check your plan’s formulary every year. During Open Enrollment (October 15-December 7), your plan can change which drugs it covers - and at what tier. Don’t assume your drug is still covered.

- Use the Medicare Plan Finder tool. Enter your exact medications and dosage. It shows you which plans cover them and how much you’ll pay. You’ll see if substitutions are likely.

- Ask your pharmacist. When you pick up a prescription, ask: “Is this the exact drug my doctor ordered, or was it swapped?” If it was swapped, ask why - and whether it’s covered under your plan’s rules.

- Keep a written note from your doctor. If you’ve had bad reactions to generics or other drugs, ask your doctor to write “Dispense as Written” or “Do Not Substitute” on the prescription.

- Know your out-of-pocket progress. Track how much you’ve spent so far this year. If you’re close to $2,000, you’re about to hit catastrophic coverage. That’s when substitution pressure drops.

What If Your Drug Gets Removed From the Formulary?

Plans can remove drugs from their formulary at any time - even mid-year. If that happens, you’ll get a notice. You have options:- Switch to an alternative drug on the formulary (if your doctor agrees).

- Request a formulary exception - your doctor files paperwork to get your drug covered anyway.

- Switch plans during a Special Enrollment Period (if you qualify).

Medicare Advantage vs. Stand-Alone Part D Plans

The way substitution works can vary depending on whether you’re on a stand-alone Part D plan or a Medicare Advantage plan with drug coverage (MA-PD). In 2025, 34 MA-PDs are available, up 143% in the last decade. These plans combine medical and drug coverage under one insurer. That means your doctor and pharmacist might be in the same network, making substitution coordination easier. But it also means your plan might have tighter control over what’s allowed. Stand-alone PDPs? There are only 14 left in 2025 - down 52% since 2015. These plans are often simpler but offer less integration. If you’re on a PDP and your doctor is outside the network, getting a substitution exception can take longer.

Who Makes the Final Call on Substitution?

It’s not just your pharmacist. It’s not just your doctor. It’s your plan’s Pharmacy Benefit Manager (PBM). PBMs are the middlemen. They negotiate drug prices, build formularies, and decide which substitutions are allowed. They’re not your doctor. They’re not your pharmacist. They’re a business. And their goal is to reduce costs - not necessarily to match your needs. That’s why you need to be proactive. Don’t wait for a surprise at the pharmacy counter. Know your plan’s rules. Know your rights. And don’t be afraid to ask for help.What’s Changing in 2026?

The $2,000 out-of-pocket cap is going up to $2,100 in 2026. That’s still a massive improvement over the old system. But it also means plans will adjust their substitution tactics to keep you just under the new threshold. Expect more use of step therapy, more prior authorizations, and more pressure to switch to generics - especially for drugs that cost over $100 per month. The Inflation Reduction Act is still being rolled out. And CMS has already released draft rules for 2026. That means substitution policies aren’t fixed. They’re evolving.Final Tip: Don’t Skip Open Enrollment

If you’re unhappy with your plan’s substitution rules, you have one main chance each year to change: Open Enrollment, October 15 to December 7. Use it. Compare plans using your exact medications. Look for one that covers your drugs on the lowest tier. Check if your plan allows therapeutic interchange without forcing you to try something risky. A small change in your plan could mean saving $500 or more - and avoiding the stress of last-minute drug switches.Can my pharmacist substitute my Medicare Part D drug without telling me?

No. Pharmacists must inform you if a substitution is made - unless your doctor wrote "Do Not Substitute" on the prescription. Even then, they’re required to explain what was swapped and why. Always ask for a printed receipt that lists the drug name and manufacturer - that’s your record.

Why does my drug cost more this year even though it’s the same?

Your plan may have moved your drug to a higher tier on its formulary. This often happens when a generic becomes available or when the plan negotiates better pricing with another brand. Check your plan’s formulary update - they’re required to send you one before the new year starts.

What if I can’t afford the substitute drug?

You can request a formulary exception. Your doctor fills out a form explaining why the substitute won’t work for you. If approved, your plan must cover your original drug. Many people get approved - especially if they’ve been stable on the original medication for months or years.

Does the $2,000 out-of-pocket cap include my monthly premium?

No. The $2,000 cap only counts what you pay for the drugs themselves - copays, coinsurance, and deductible amounts. Your monthly premium doesn’t count toward this cap. Only the money you spend at the pharmacy counts.

Can I switch plans mid-year if my drug gets dropped?

Yes - if your plan removes a drug you’re taking, you qualify for a Special Enrollment Period. You have 60 days to switch to another Part D plan that covers your medication. Don’t wait - once you’re without coverage, you risk running out of medicine.

Randall Little

So let me get this straight - the government capped out-of-pocket costs at $2,000, but the PBMs are still playing chess with our prescriptions like we’re pawns in a corporate game of Monopoly? Brilliant. Just brilliant. I’ve had my insulin swapped twice this year - both times to a ‘therapeutically equivalent’ brand that gave me a rash. Turns out ‘equivalent’ in PBM-speak means ‘cheaper and less likely to land me in the ER.’

And don’t get me started on the ‘Do Not Substitute’ scrip. My doctor wrote it in triplicate. The pharmacist still swapped it. Said the system ‘automatically overrides.’ No one’s accountable. Just a bunch of algorithms deciding if I live or die based on quarterly profit margins.

Rosalee Vanness

I just want to say - if you’re reading this and you’re scared about your meds changing, you’re not alone. I spent three months in 2023 panicking because my antidepressant got moved to Tier 4. I cried in the pharmacy parking lot. I called my doctor three times. I even wrote a letter to my plan. And you know what? They denied it. But I didn’t give up. I appealed. I had my doctor write a 12-page letter detailing how my anxiety spiked every time I tried the ‘alternative.’ And guess what? They approved it. It took 47 days. I was out of pills for a week. But I won. You can too. Don’t let them make you feel like your health is just a line item.

And if you’re lucky enough to have a pharmacist who actually takes the time to explain the swap? Hold onto them. They’re rare. My pharmacist, Brenda, keeps a sticky note on her counter with my name and ‘NO SUBSTITUTES - PATIENT HAS SEIZURE RISK.’ She’s my hero.

mike swinchoski

People are making this way too complicated. Just take the cheap pill. You’re not special. Your body isn’t that delicate. If the generic works for 90% of people, it’ll work for you. Stop whining. The system’s not out to get you - you’re just lazy. Get off your butt and learn how to read a formulary. It’s not rocket science. It’s a PDF.

Trevor Whipple

bro i just had my omeprazole swapped for esomeprazole and now i got the worst headache of my life. i called the pharmacy and they were like ‘oh that’s the same thing’ no it’s not bro it’s not the same thing. my doc wrote ‘do not substitute’ but the system overrode it. i’m filing a complaint. also why is my premium going up again? this is a scam. also my cat has diabetes now too so i’m broke. help.

Lethabo Phalafala

Let me tell you something - I come from a country where you pay for medicine with your dignity. Here, you pay with your life. I watched my aunt die because her blood pressure med was swapped for a cheaper version she couldn’t metabolize. She didn’t even know until her kidneys gave out. This isn’t about savings. This is about who gets to live and who gets to be a statistic. And if you think this is normal - you’re not paying attention.

Don’t wait for the letter. Don’t wait for the notice. Call your plan. Demand your formulary. Print it. Highlight your drugs. Take it to your doctor. Make them see you. You are not a cost center. You are a human being. And you deserve better.

Damario Brown

so here's the real tea: PBMs make more money when you stay on brand name drugs because they get kickbacks from pharma. so why would they push generics? they wouldn't. unless the brand just got a patent expiry and they can now negotiate a 70% discount on the generic. then they'll shove it down your throat like it's a miracle. but if the brand is still under patent? they'll make you jump through 17 hoops to get it. it's not about cost - it's about profit margins. and your health? that's just the collateral damage.

also - why is no one talking about how the $2k cap only counts what YOU pay? not what the plan pays? so if your drug costs $500/month and you pay $50 - that's $600/year. you're still 1400 away from the cap. they're not helping you - they're just moving the goalposts.

John Pope

There’s a metaphysical layer to this, you know. The substitution of pharmaceuticals is merely a symptom of the broader ontological crisis of commodified care. We’ve reduced the human body to a variable in a supply-chain algorithm. Your insulin isn’t medicine - it’s a line item. Your hypertension isn’t illness - it’s a risk profile. We’ve outsourced healing to actuaries who’ve never held a stethoscope. And yet - we call this ‘efficiency.’

The real tragedy isn’t the swap. It’s that we’ve stopped asking: Who authorized this? Who gave them the right to decide which body gets to heal - and which one gets to be optimized?

Adam Vella

It is imperative to underscore that the structural framework governing Medicare Part D substitution is predicated upon evidence-based formulary management protocols established by the Centers for Medicare & Medicaid Services. The utilization of therapeutic interchange, while occasionally perceived as adversarial, is in fact a clinically validated mechanism for cost containment without compromising therapeutic outcomes. Furthermore, the implementation of the $2,000 out-of-pocket cap represents a significant advancement in beneficiary financial protection, thereby reducing the incentive for premature substitution in the catastrophic phase. Beneficiaries are strongly advised to consult their plan’s official formulary documentation, which is accessible via the Medicare.gov portal, prior to initiating any medication changes.

Alan Lin

As a former Medicare plan administrator, I’ve seen the inner workings of PBMs - and I’m here to tell you: most of the time, the pharmacist doesn’t even know why the substitution happened. The system auto-flags your prescription based on tier shifts, and the pharmacy’s software pushes the cheapest option without human review. I’ve seen patients on insulin get swapped to a different brand that required a 30% higher dose - and no one caught it until they were in the ER. That’s not a system failure. That’s a design flaw.

Here’s what you must do: Every time you pick up a prescription, ask for the original drug name and the dispensed drug name. Write it down. If they’re different, call your plan immediately. Don’t wait. Your doctor can’t fix this after the fact. Only you can stop it before it happens.

And if your plan denies your exception request? File a Level 1 Appeal. Then a Level 2. Then escalate to CMS. Over 60% of appeals are approved when they’re properly documented. You are not powerless. You just need to be relentless.